How Much Stamp Duty Will You Pay?

Stamp duty is one of the largest upfront costs when buying a home in England or Northern Ireland, yet many buyers are unsure how much they owe or whether they qualify for relief. This guide explains the current rates from April 2025, how the banded system works, and what first-time buyers and additional property owners need to know.

Stamp Duty Land Tax is one of the biggest upfront costs involved in buying a property in England or Northern Ireland. Yet it is also one of the least understood. Many buyers are caught off guard by the amount they owe, or miss out on reliefs they are entitled to, simply because they did not plan ahead.

This guide explains everything you need to know about how stamp duty works, what the current rates are, who qualifies for relief, and how to work out your own liability before you buy. It covers the rules that have applied since April 2025 and cuts through the confusion so you can budget with confidence.

If you want to calculate your exact liability right now, use the free Stamp Duty Calculator on YooSell.

What Is Stamp Duty Land Tax

Stamp Duty Land Tax, commonly known as stamp duty, is a tax paid by the buyer when purchasing property or land above a certain price in England and Northern Ireland. It applies to freehold properties, leasehold properties, new builds, shared ownership homes, and land transactions.

Scotland and Wales have their own versions of the tax. Scotland uses Land and Buildings Transaction Tax and Wales uses Land Transaction Tax. The rates and thresholds in those countries differ from those covered in this guide, which focuses on England and Northern Ireland.

Stamp duty is calculated on the purchase price you pay. It is not a flat rate applied to the whole amount. Instead, it works in bands, meaning you only pay each rate on the portion of the price that falls within that band. This is similar to how income tax works.

When Do You Have to Pay Stamp Duty

You are required to pay stamp duty within 14 days of completing your property purchase. Your solicitor or conveyancer will almost always handle the SDLT return and payment to HMRC on your behalf as a standard part of the conveyancing process. If you are handling the transaction yourself without a solicitor, it remains your legal responsibility to file and pay on time.

Missing the 14-day deadline results in financial penalties and interest charges from HMRC. This is another reason most buyers use a qualified conveyancer who manages this automatically.

Who Pays Stamp Duty

Stamp duty is always paid by the buyer, not the seller. There is no equivalent transaction tax for sellers in England and Northern Ireland, though sellers are responsible for other costs such as legal fees, estate agent fees, and removal costs.

In some negotiations, a seller may agree to contribute towards a buyer's stamp duty as part of agreeing a sale, but this is a matter of private arrangement between the parties and does not change the legal obligation, which remains with the buyer.

Current Stamp Duty Rates in England and Northern Ireland

The current rates have applied since 1 April 2025, when the temporary thresholds introduced in September 2022 came to an end. The rates below apply to completions from that date onwards.

Standard Residential Rates

These rates apply to buyers who are purchasing a main residential property and are not first-time buyers or buying an additional property.

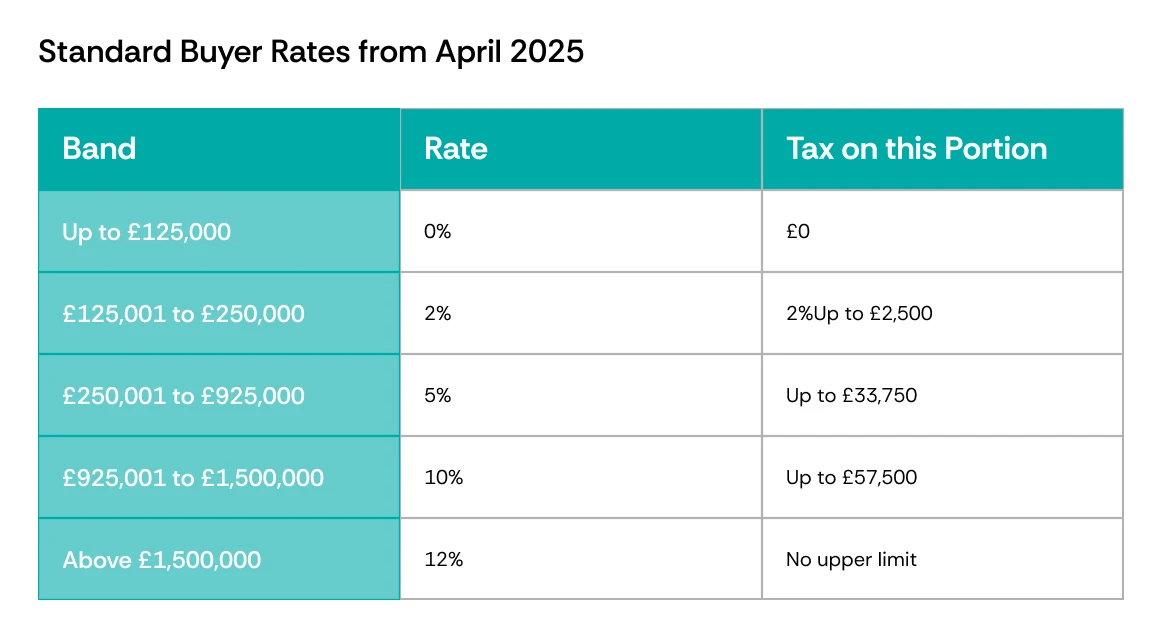

Standard Buyer Rates from April 2025

Because stamp duty is charged on each portion separately, a buyer purchasing a property at £300,000 does not pay 5% on the full amount. They pay 0% on the first £125,000, 2% on the next £125,000, and 5% only on the remaining £50,000. The total in that example comes to £5,000.

First-Time Buyer Relief

First-time buyers in England and Northern Ireland benefit from a reduced rate on their purchase, provided the property costs no more than £500,000. This relief has applied in its current form since April 2025 after the temporary higher thresholds introduced in 2022 were removed.

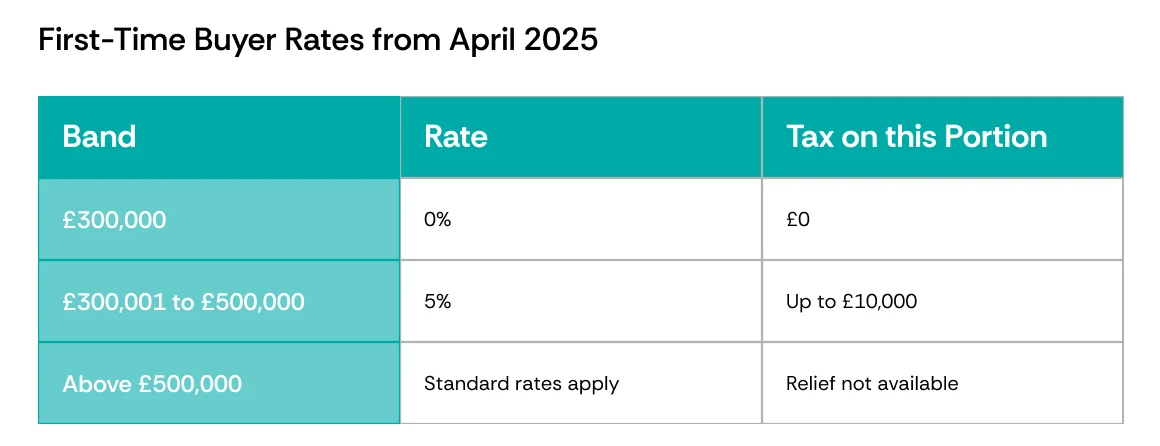

First-Time Buyer Rates from April 2025

A first-time buyer purchasing a property at £280,000 pays no stamp duty at all. A first-time buyer purchasing at £400,000 pays 5% only on the £100,000 above the £300,000 threshold, which equals £5,000.

If the purchase price exceeds £500,000, no first-time buyer relief is available and the standard rates apply in full.

Additional Property Surcharge

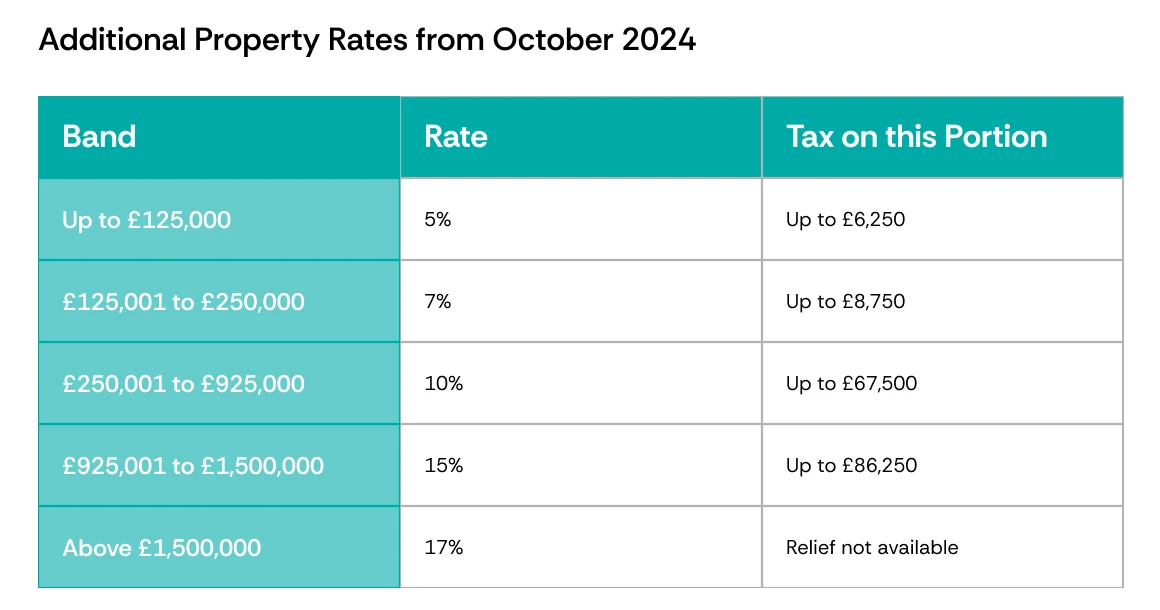

If you are purchasing a second home, a buy-to-let property, or any residential property you will own in addition to your main home, an additional surcharge applies. From 31 October 2024, this surcharge increased to 5 percentage points above the standard rates on every band.

Additional Property Rates from October 2024

The additional property surcharge applies even if you are in the process of selling your main home at the time of purchase. However, if you sell your previous main home within three years of buying the new one, you can apply to HMRC for a refund of the surcharge.

Non-UK Resident Surcharge

Buyers who are not UK residents at the time of purchase pay an additional 2% surcharge on top of all other applicable rates. This surcharge was introduced in April 2021 and applies to both standard buyers and those already subject to the additional property surcharge. The YooSell Stamp Duty Calculator includes a toggle for non-UK resident buyers so you can calculate your correct liability.

Who Qualifies as a First-Time Buyer for Stamp Duty Purposes

The definition used by HMRC is specific and it is worth understanding before you assume you qualify. A first-time buyer is someone who has never previously owned a freehold or leasehold interest in a residential property anywhere in the world. This includes properties owned abroad as well as in the UK.

Situations That May Affect Eligibility

There are a number of circumstances that can affect whether you qualify for first-time buyer relief.

• Inheriting a property, even a share of one, may count as having owned a residential interest and could disqualify you from relief

• If you are buying jointly, all buyers must qualify as first-time buyers for the relief to apply. If one buyer has previously owned a property, the relief is not available

• Owning a commercial property, such as a shop or office, does not disqualify you from first-time buyer relief, as HMRC's definition specifically relates to residential interests

• Having previously owned property and sold it does not restore your first-time buyer status

If you are unsure whether you qualify, speak to your solicitor or conveyancer before proceeding. Incorrectly claiming relief and underpaying stamp duty can result in penalties from HMRC.

How Stamp Duty Is Calculated in Practice

One of the most common sources of confusion about stamp duty is the misunderstanding that the rate shown for a purchase price applies to the whole amount. It does not. Stamp duty is a progressive, banded tax, meaning each rate applies only to the slice of the price that falls within that band.

A Worked Example for a Standard Buyer

A standard buyer purchasing a property at £350,000 in England from April 2025 would calculate their liability as follows.

• 0% on the first £125,000 equals £0

• 2% on the next £125,000 (from £125,001 to £250,000) equals £2,500

• 5% on the remaining £100,000 (from £250,001 to £350,000) equals £5,000

• Total stamp duty owed: £7,500

A Worked Example for a First-Time Buyer

A first-time buyer purchasing a property at £350,000 would calculate their liability differently.

• 0% on the first £300,000 equals £0

• 5% on the remaining £50,000 (from £300,001 to £350,000) equals £2,500

• Total stamp duty owed: £2,500

The first-time buyer in this example saves £5,000 compared to a standard buyer on the same property. This saving is significant and it is one reason why understanding your status before making an offer matters.

A Worked Example for an Additional Property Buyer

A buyer purchasing a second property or buy-to-let at £250,000 would pay at the additional property rates.

• 5% on the first £125,000 equals £6,250

• 7% on the next £125,000 (from £125,001 to £250,000) equals £8,750

• Total stamp duty owed: £15,000

Rather than working through the calculation manually, use the free Stamp Duty Calculator on YooSell to get an instant breakdown for any purchase price, buyer type, and residency status.

Stamp Duty in Scotland and Wales

If you are buying property in Scotland or Wales, different taxes apply. This is important to understand because searches for stamp duty information often return results based on English rates, which will give you an incorrect figure if you are buying outside England or Northern Ireland.

Land and Buildings Transaction Tax in Scotland

Scotland replaced stamp duty with its own Land and Buildings Transaction Tax in April 2015. The rates, thresholds, and reliefs differ from those in England. If you are buying in Scotland, the rates in this guide do not apply to you and you should refer to the Scottish Government's official guidance or speak to a Scottish conveyancer.

Land Transaction Tax in Wales

Wales introduced its own Land Transaction Tax in April 2018. Again, the rates and structure differ from England and Northern Ireland. If you are buying in Wales, the SDLT rates in this guide are not relevant to your purchase. A Welsh conveyancer or the Welsh Revenue Authority's official guidance will give you the correct figures.

Other Stamp Duty Reliefs and Exemptions

Beyond first-time buyer relief, there are a number of other situations where stamp duty is reduced or not applicable.

Properties Below the Threshold

No stamp duty is owed on any residential property purchased for £125,000 or less by a standard buyer. For first-time buyers, no stamp duty is owed on properties up to £300,000. If the purchase price falls at or below these thresholds, an SDLT return still needs to be filed with HMRC even if nothing is owed, unless an exemption applies.

Transfers as Part of Divorce or Dissolution of a Civil Partnership

Where property is transferred between former spouses or civil partners as part of a divorce settlement or dissolution, SDLT is generally not charged. This is a specific legal relief and the exact circumstances need to be confirmed with a solicitor.

Inherited Property

Inheriting a property does not trigger a stamp duty liability because there is no purchase taking place. However, if you later purchase a property while owning an inherited one, the inherited property may count towards additional property surcharge calculations.

Shared Ownership Schemes

Buyers purchasing through a shared ownership scheme have two options for calculating their stamp duty. They can pay on the full market value of the property at the point of first purchase, or they can pay only on the initial share they are buying and then pay further amounts as they staircase to a larger share. Each option has implications for the total tax paid and your conveyancer should advise you on which approach suits your circumstances.

Stamp Duty on Leasehold Properties

Buying a leasehold property works slightly differently for stamp duty purposes. In addition to the standard SDLT on the purchase price of the lease, there may be an additional charge based on the rent paid over the life of the lease.

Where the total rent over the life of the lease, calculated using a net present value method, exceeds £125,000, stamp duty is charged at 1% on the portion that exceeds that threshold. This additional charge is separate from the SDLT payable on the purchase price itself.

Most buyers of leasehold properties, particularly residential flats, find this does not result in a significant additional charge, but it is worth discussing with your conveyancer to make sure nothing is missed.

Planning for Stamp Duty When Buying a Property

Stamp duty cannot be added to your mortgage in most cases. Lenders generally require it to be paid from your own funds at completion. This makes it an important part of your upfront budget and something to factor in well before you start making offers.

Include It in Your Total Buying Costs

When budgeting for a property purchase, stamp duty sits alongside solicitor fees, survey costs, and any mortgage arrangement fees as part of your upfront costs. Failing to account for it can leave buyers short of funds when they reach completion, which can delay or jeopardise a sale.

Factor It Into Your Offer Strategy

Knowing your stamp duty liability before you make an offer helps you understand the true total cost of a purchase. This is particularly relevant when you are comparing two properties at different price points. A small difference in asking price can produce a meaningful difference in stamp duty, especially around band thresholds.

The Cost Saving Calculator on YooSell can also help you understand how selling through YooSell rather than a traditional agent affects your overall financial position when moving to a new home.

Stamp Duty Around Band Thresholds

The banded structure of stamp duty means that buying just above certain price points can result in a noticeably higher tax bill. For example, a buyer purchasing at exactly £125,000 pays no stamp duty. A buyer purchasing at £126,000 pays 2% on the £1,000 above the threshold, which is a very small amount. But understanding these thresholds becomes more significant at higher prices.

At the £250,000 mark, the rate moves from 2% to 5% on the portion above that figure. A buyer at £251,000 pays 5% on £1,000 rather than 2%. While this is a minor difference on one small portion, these thresholds are worth knowing when negotiating a final price.

Selling Your Home with YooSell

If you are selling your current home and buying a new one, understanding your stamp duty position on the purchase is just one part of the financial picture. The amount you save on your sale can directly affect how comfortably you meet those buying costs.

Why Sellers Choose YooSell

Traditional estate agents typically charge a percentage commission on your sale price. YooSell works on a fixed monthly fee with no commission taken at completion. For many sellers, particularly those selling a higher-value home, the saving is substantial and can comfortably cover stamp duty and other buying costs on their onward purchase.

See exactly how much you could save using the Cost Saving Calculator on the YooSell website.

Tools to Help You Plan Your Move

YooSell provides a range of free calculators to help you plan your property transaction. The Stamp Duty Calculator covers standard, first-time buyer, and additional property rates from April 2025, including the non-UK resident surcharge. The Valuation Calculator helps you understand what your home is currently worth, and the Mortgage Calculator lets you estimate your monthly repayments on a new purchase.

List on Rightmove Through YooSell

You can list your property directly on Rightmove through YooSell, giving your home exposure on the UK's largest property portal and helping you attract verified, serious buyers. Find out more on the YooSell Rightmove page.

To understand how the full process works and which plan suits your sale, visit the How It Works page or explore the pricing options.

Frequently Asked Questions

Read Our Blog

Tips, insights and expert advice to help you sell smarter.

Buy-to-Let Exit Strategies: What Every UK Landlord Should Know in 2026

93,000 landlords exited in 2025. Section 21 is gone. CGT exemptions are lower than ever. Here is every exit route for UK landlords in 2026, what each costs, and how to keep as much of your money as possible.

How long on average it takes to sell a house in the UK?

Average UK sale time: 3 months. Average agent fee on a £500k home: £12,000. Those two facts belong in the same conversation. Here's the full 2026 timeline, and how a fixed fee changes everything.

Why Sell Your House Yourself? Here's What the Estate Agents Don't Tell You

Estate agents charge 1.42% commission on average. On a £280,000 home, that's over £5,000 of your money. Here's exactly why selling your house yourself in 2026 makes sense, and how to do it properly.

Start Selling Your Home Today!

Take control of your sale with YooSell. Get started today and explore how we can help you sell smarter, faster, and with less hassle.