|Reading time: 11 minutes

UK Housing Market Forecast 2026–2027: Should You Buy, Sell or Wait?

The UK housing market forecast for 2026–2027 points to modest price growth in affordable regions, downward pressure in London and the South East, and continued uncertainty driven by elevated mortgage rates. Most credible forecasters now expect national house prices to move between -2% and +2% across 2026, with a gradual recovery taking shape from 2027 onwards. If you're trying to decide whether to buy, sell or wait, the honest answer is: it depends entirely on where you are, what type of property you're dealing with, and how long your timeline is.

That probably isn't the clean yes or no you were hoping for. But after years of working with sellers across the Midlands and beyond, I can tell you that the people who make the best property decisions are the ones who understand the market clearly rather than waiting for a perfect moment that rarely comes. This guide pulls together the latest UK housing market forecast data from Savills, Knight Frank, Rightmove, Nationwide, and the House of Commons Library, and translates it into practical guidance for buyers and sellers in 2026 and into 2027.

What Does the UK Housing Market Forecast for 2026 Actually Say?

The UK housing market forecast for 2026 is more divided than any year in recent memory. At the start of the year, major forecasters predicted modest positive growth of 2-4%. The outbreak of conflict in the Middle East in early 2026 changed that picture significantly, pushing inflation higher and causing fixed mortgage rates to spike before gradually falling back.

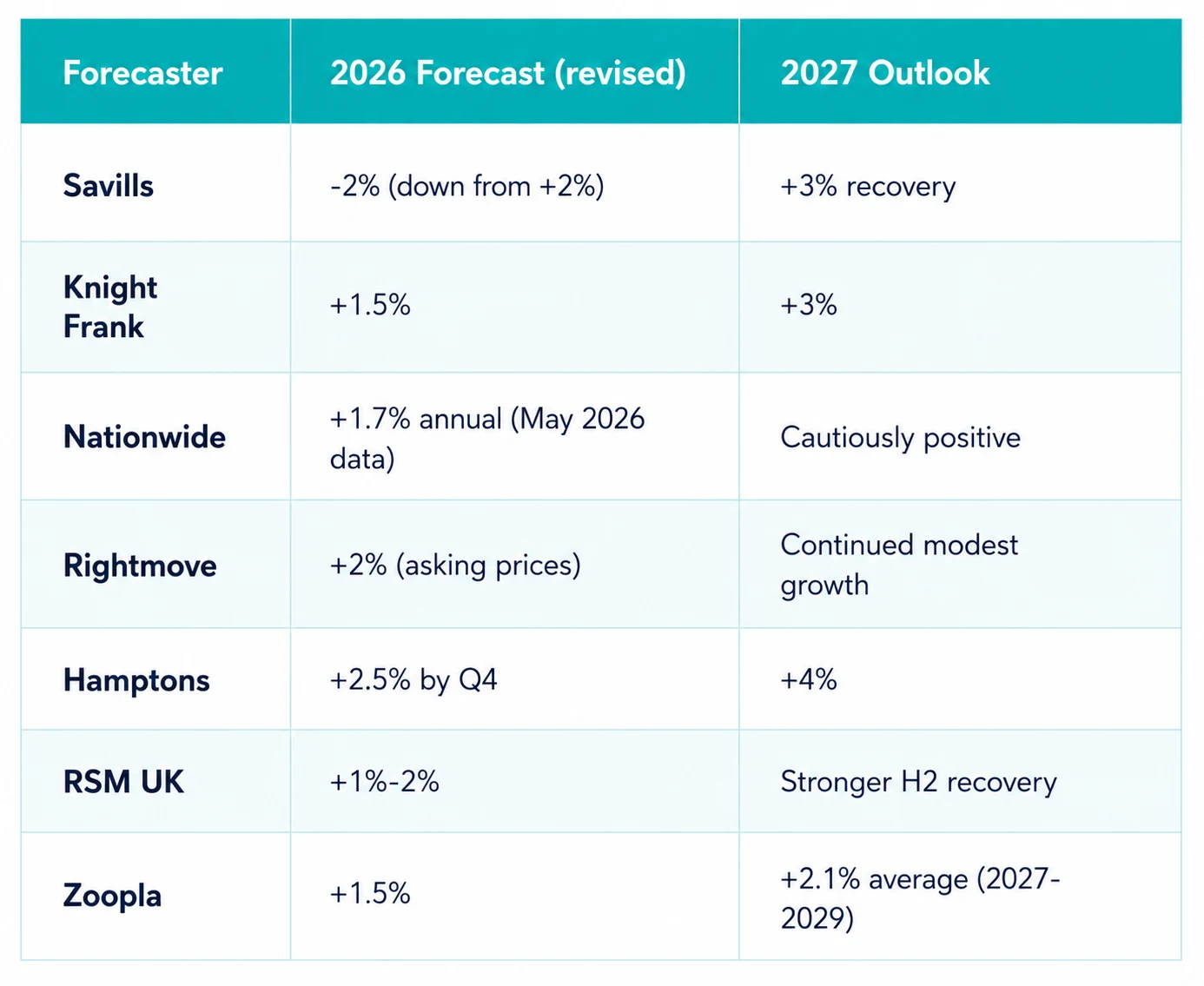

Here is where the major forecasters currently stand as of mid-2026:

According to the UK House Price Index published by the House of Commons Library, house prices increased by 3.8% in the year to April 2026 on a seasonally adjusted basis, with average prices up 0.6% between March and April 2026. That headline figure masks enormous regional variation, which is where the real story lies.

The UK housing market forecast is best understood as a tale of two markets: affordable northern regions and the Midlands pushing upward, and London and the South East under measurable pressure.

Why Are House Prices Behaving Differently Across the UK?

Regional divergence in the UK housing market is not new, but in 2026 it's more pronounced than it's been in a decade.

RSM UK's housing tracker found that regions including the North West, Yorkshire and Humber, and the West Midlands may see price increases of 3-4%, while London and much of the South East will see minimal increases. Northern Ireland is an outlier, with potential growth of up to 5%.

The reason comes down to affordability. Where house prices are lower relative to local earnings, buyers can still absorb modestly elevated mortgage rates and transact. Where prices are high relative to earnings, particularly in London and the South East, every basis point of mortgage rate increase knocks another tranche of buyers out of the market.

Lucian Cook, head of residential research at Savills, noted that "lower demand is being set against elevated levels of stock, partially from landlords selling up in the face of greater regulation, which will place downward pressure on prices, particularly across submarkets in London and the South East."

For sellers and buyers in the East Midlands and Leicestershire specifically, this is encouraging news. The Midlands sits in the more resilient half of the UK market right now. Browse current properties listed in your area on YooSell to get a live sense of local supply and demand.

What's Driving the North-South Divide?

Three factors are doing most of the work:

Affordability headroom. In the North West and Midlands, average earnings-to-house-price ratios remain more manageable than in the South, giving buyers more room to act even at current mortgage rates.

Landlord exits. An estimated 220,000 fewer rental homes are expected by the end of 2026 as private landlords exit in response to regulatory and tax changes. Where landlords sell, stock increases and buyers gain negotiating power, but this effect is particularly concentrated in London.

New-build pipeline. House building starts in England rose 23% quarter-on-quarter in Q4 2025 and 24% year-on-year, which will add supply gradually through 2027. More supply in the right locations helps buyers; less supply elsewhere supports seller pricing.

What's Happening to Mortgage Rates in 2026?

Mortgage rates are the single biggest variable in the UK housing market forecast right now, and they've moved more than most predicted.

According to the HomeOwners Alliance's June 2026 mortgage rate forecast, the Bank of England held interest rates at 3.75% for the fourth consecutive time on 18 June 2026, following the US-Iran ceasefire and lower-than-expected inflation data for May. That's broadly positive news, but mortgage rates remain elevated compared to the start of 2026.

As of 17 June 2026, the average two-year fixed mortgage rate stands at 5.60% and the average five-year fix at 5.58%, according to Which?, with very few sub-4% deals still available.

The practical implication for buyers is this: the cost of borrowing remains high enough that affordability is genuinely stretched in higher-price areas. For sellers, it means the pool of active, mortgage-ready buyers is smaller than it was in 2021-2022, and pricing accuracy matters more than ever.

Oxford Economics believes the Bank of England will hold interest rates at their current level for the rest of 2026 and "well into 2027," though Pantheon Macroeconomics' chief economist Rob Wood noted that the drop in oil prices following the US-Iran ceasefire had already led his team to remove a forecast rate hike.

For sellers thinking about timing, a clearer rate trajectory in H2 2026 or early 2027 could bring more buyers back to the market, improving both speed and final price. Use YooSell's Mortgage Calculator to stress-test what current rates mean for your own situation.

Should You Sell Your House in 2026 or Wait Until 2027?

Selling in 2026 still makes strong financial sense for most Midlands and northern England homeowners, provided you price correctly from the start. Waiting until 2027 offers a potentially better rate environment, but not a dramatically higher price.

This is one of the questions I get most often from homeowners in Leicestershire and the surrounding area. And my answer is always the same: the "perfect time to sell" is the moment that aligns with your personal situation, not a point on a forecast chart.

That said, here's what the data supports:

The case for selling now (mid-2026):

Mortgage approvals in April 2026 were up 9% year-on-year, with 65,945 approvals compared to 60,510 in April 2025, signalling genuine buyer activity despite rate headwinds.

Rightmove reports sellers are currently taking an average of 60 days to secure a buyer, which is not dramatically longer than the long-run average.

Stock levels are elevated, meaning buyers have choice. But that also means well-priced, well-presented properties are standing out more clearly from the crowd.

If you're simultaneously buying, locking in your purchase before potential 2027 price recovery means buying into a market that hasn't rebounded yet.

The case for waiting until 2027:

Knight Frank forecasts UK house price growth of 1.5% in 2026 followed by 3% in 2027, so waiting 12 months could mean a modestly higher sale price.

Savills' longer-term forecast projects 4% growth in 2027 and 5% in 2028, with much of the medium-term recovery expected in the back half of the forecast window.

Mortgage rates may ease, widening the pool of buyers who can afford your property.

The counterpoint to waiting: if you're paying agent fees, mortgage interest, or simply deferring a life decision (upsizing, downsizing, relocating), the cost of waiting can easily cancel out a 1-2% gain in theoretical value.

Use YooSell's free Valuation Calculator to get a current estimate of what your property is worth in the 2026 market, and run your numbers through the Cost Saving Calculator to understand what you'd net after fees before making any decision.

Is Now a Good Time to Buy a House in the UK?

For first-time buyers and those with genuine housing needs, 2026 is a reasonable time to buy in affordable regions of the UK. For discretionary buyers in London or the South East, waiting for rate stabilisation may make more sense.

The case for buying now in the Midlands and North is actually fairly compelling. Here's why:

Rightmove data shows that peoples' incomes are expected to grow faster than property prices in 2026, which will gradually improve the balance between earnings and housing costs, particularly benefiting first-time buyers saving for deposits.

Stock at a decade high means buyers have real negotiating leverage, something that was genuinely absent in 2021-2022.

House prices are expected to grow by 22% in the five years to 2030 according to RSM UK, meaning buyers who enter the market now are positioned to benefit from medium-term appreciation.

Timing the perfect entry point is notoriously unreliable. As the saying goes in property: it's time in the market, not timing the market.

The key risk for buyers in 2026 is overpaying in areas where Savills and Knight Frank are forecasting near-term price softness, namely prime London, the South East, and premium rural markets. In those locations, patient buyers may get a better deal in late 2026 or early 2027.

Read YooSell's Area Guides for a neighbourhood-level view of the Leicestershire and Midlands market.

What Does the UK Housing Market Slowdown Mean for Sellers?

A housing market slowdown does not mean it's a bad time to sell. It means the strategy for selling needs to change.

In a rising market, even overpriced properties eventually find a buyer. In a slower market, pricing accuracy and presentation become the difference between a quick sale at a good price and months of stagnation with repeated reductions.

Here is what works in a slower market:

Price from sold data, not aspirational asking prices. Comparable sold prices in the past three to six months are your most reliable guide. Use YooSell's Valuation Calculator and cross-reference with HM Land Registry sold prices to anchor your price in reality.

Present the property properly. Professional photography, a clear floor plan, and a well-written description do more in a competitive market than they did when buyers were desperate. YooSell's listing tools include AI-assisted descriptions and an integrated viewings system.

Minimise your selling costs. In a flat market, every pound saved on fees is a pound in your pocket. A 1.42% estate agent commission on a £280,000 property is nearly £4,000. Selling through YooSell from £49.50 per month keeps that money with you.

Be responsive. Buyers in a well-stocked market will move on if they don't hear back promptly. Quick responses to enquiries and flexible viewing times make a measurable difference to offer rates.

How Does the 2026 Forecast Compare to Previous Market Slowdowns?

Context matters when reading a UK housing market forecast. Is 2026 a blip or the beginning of something more structural?

The honest answer is that 2026 looks more like a managed correction than a crash, and very different from 2008.

In 2008-2009, house prices fell 15-20% nationally, driven by a credit crisis that cut off mortgage supply almost entirely. Today's market has structural protections that didn't exist then: widespread fixed-rate mortgage adoption means most homeowners are insulated from rate rises until their deal expires; lending criteria are significantly tighter than pre-2008; and unemployment remains relatively low.

Savills noted that "stricter mortgage regulation and the widespread use of fixed-rate mortgages continue to keep the risk of forced sales low," describing the expected adjustment as "a modest adjustment in nominal house prices."

The 2022-2023 slowdown following the Truss/Kwarteng mini-budget is a closer parallel. Prices fell 4-5% nationally before recovering. The current slowdown appears shallower. Q1 2026 completions reached 269,000, around 30,000 below the five-year quarterly average, which shows a quieter market but not a seized one.

For most long-term homeowners, these fluctuations matter less than the trajectory. Savills forecasts 18.5% cumulative growth over the five years to 2030, suggesting the medium-term direction is clearly upward even if the 2026 path is bumpy.

Read YooSell's Property Guides for practical advice on preparing your home for sale in any market condition.

Conclusion

The UK housing market forecast for 2026-2027 tells a story of genuine regional divergence, elevated but stabilising mortgage rates, and a market that rewards smart, well-prepared sellers more than ever before. The national headline is modest: most credible forecasters now expect flat to slightly negative national prices in 2026, followed by a clearer recovery from 2027 onwards. But that national number is almost meaningless for an individual seller or buyer. What matters is your specific property type, your local area, and your personal timeline.

For sellers in the Midlands and northern England, the fundamentals are more supportive than the headlines suggest. Buyer activity, measured in mortgage approvals, is running 9% ahead of last year. Stock is elevated but not overwhelming. And in a market where buyers have more choice, the sellers who price accurately and present their property well are consistently outperforming those who don't.

For buyers, 2026 offers a genuine opportunity in affordable markets. Earning power is outpacing house prices in real terms. Choice is at a decade high. Medium-term forecasts point consistently to significant growth through 2030. The risk of waiting for a "better time" is that better times arrive with higher prices and less choice.

Whatever you decide, your strategy should start with data, not emotion. Know what your home is worth today. Know what comparable properties have actually sold for. Know what you'd net after every fee.

Here is your clear next step. Run your property through YooSell's free Valuation Calculator to see what it's worth in the current market. Then check your potential saving with the Cost Saving Calculator. When you're ready to list, register on YooSell and sell on your terms, with no commission, no pressure, and full control of the process.

The market will always be uncertain. Your decision doesn't have to be.

Frequently Asked Questions

Start Selling Your Home Today!

Take control of your sale with YooSell. Get started today and explore how we can help you sell smarter, faster, and with less hassle.